Having a good credit score is important. It can help you get approved for personal loans, mortgages, credit cards, and other financial products. And it can even help you get better interest rates on those products.

There are a lot of ways to build your credit score. You can make sure you always pay your bills on time, keep your balances low, and avoid opening too many new accounts at once.

But there's one more way to give your credit score a boost: using credit building apps. These apps can help you track your progress, stay on top of your payments, and even find new opportunities to build your credit.

Would you benefit from a higher credit score? If so, here are the best credit builder apps to use.

Best Credit Boosting Apps to Improve Your Credit Score

There are a number of credit building apps available that can help you improve your credit score. Here are some of the best:

1. Kikoff – Best for low $5 monthly fee

Overview

With Kikoff, you can build your credit score affordably. This credit building app helps people build credit with no credit pull required at only $5 a month. It's easy to get started, simply sign up for an account and you will be instantly approved and able to start using the credit building services that same day. There is no credit check required, which is nice.

Then, you’ll have a $750 line of credit to use in the Kikoff store. This doesn’t expire, so you can continue building your credit on your schedule. Choose from a variety of items from the store such as self-help eBooks starting at just $10. You’ll be able to make your purchase with your newly created Kikoff Credit Account. Every on-time payment you make will help you build your credit. All it takes is one click—and they’ll send you reminders to make sure.

Why we choose it

As a Kikoff customer and user, you'll be entitled to a $750 credit line that can be used whenever needed. With Kikoff, your payment history is reported to the three credit bureaus, which can enhance your credit score.

The best thing about apps like Kikoff is that it doesn't require a credit check and you'll only have to pay $5 a month, there's not much stopping you from building credit for a low monthly fee. It has affordable plans and utilizes credit more efficiently, making it a good option for building credit.

Keep in mind that your credit score will not be affected by signing up, and there are no hidden fees. In addition, Kikoff comes with a mobile app, making it user-friendly to use.

Pros

- No credit check required so most people can be approved

- Products in the store are relatively cheap

- Monthly minimum payment is only $5

Cons

- Must purchase an item through the proprietary store which only includes self-help eBooks

Pricing

Depending on your needs, Kikoff offers 2 products, both products report to the major credit bureaus and are offered as 1-year plans:

- Kikoff Credit Account – the standard product for all new Kikoff customers. This account builds monthly payment history and helps reduce your credit utilization. The Credit Account gets reported to Equifax and Experian every month and costs $5/month.

- Kikoff Credit Builder Loan – this is an optional add-on for customers that want to build even more credit. This is a 1-year savings plan for $10/month. You’ll be able to add this product after your first payment with the Kikoff Credit Account.

Kikoff is the only credit building program intentionally designed to keep your utilization rate low so you can build credit easily.

- No credit check required so most people can be approved

- Products in the store are relatively cheap

- Monthly minimum payment is only $5

- Must purchase an item through the proprietary store which only includes self-help eBooks

2. Self – Best credit builder loan

Self offers a credit building app that helps build positive payment history by opening a Credit Builder Account. Once you have opened a Credit Builder Account your monthly payments are reported to all three credit bureaus.

Why we choose it

Credit Builder Accounts like the ones offered by Self can be good for establishing credit since they don’t do a hard credit pull on your credit report. Self also offers customers the ability to track their credit score via mobile app and web.

Pros

- You choose your monthly payment from 4 options

- Credit check is not required

- Reports to each of the three credit bureaus

Cons

- One missed payment may adversely affect your credit score

- Savings are not available until the account is paid off

- While it may help you build credit, you should also focus on other aspects of your credit

Pricing

The 4 different plan options vary with monthly payments of between $25 and $150. An non-refundable administrative fee of $9 is charged at account origination. You will be required to make monthly payments to your account in the amount selected until the plan is complete. You can see the pricing page here.

By opening a Self Credit Builder Account and paying monthly, on-time, you can build positive payment history. This can lead to a better credit score.

- You choose your monthly payment from 4 options

- Credit check is not required

- Reports to each of the three credit bureaus

- One missed payment may adversely affect your credit score

- Savings are not available until the account is paid off

- While it may help you build credit, you should also focus on other aspects of your credit

*Sample products: A loan with a $25 monthly payment, 24 month term with a $9 admin fee at a 15.92% Annual Percentage Rate with a finance charge of $89. Refer to www.Self.inc/pricing for current pricing.

**All Credit Builder Accounts made by Lead Bank, Member FDIC, Equal Housing Lender, Sunrise Banks, N.A. Member FDIC, Equal Housing Lender or SouthState Bank, N.A. Member FDIC, Equal Housing Lender. Subject to ID Verification. Individual borrowers must be a U.S. Citizen or permanent resident and at least 18 years old. Valid bank account and Social Security Number are required. All loans are subject to consumer report review and approval. All Certificates of Deposit (CD) are deposited in Lead Bank, Member FDIC, Sunrise Banks, N.A., Member FDIC or SouthState Bank, N.A., Member FDIC.

3. Sky Blue Credit – Best for credit repair services

With Sky Blue Credit repair, you're in charge. You can take advantage of valuable services like credit disputes and credit score assistance — while rebuilding your credit score — all with the help of expert coaching sessions. Sky Blue Credit has been in the credit repair business for many years. They have earned a reputation for excellent customer service.

Why we choose it

Sky Blue may help you meet your credit repair needs because the company takes a comprehensive look at your credit history to identify any items that could be disputed. It also claims to be able to help you dispute them faster than if you were doing it on your own. In addition, Sky Blue can assist you with debt collectors and preparing for a home purchase.

With their customer-oriented program, you get the lowest reviewed monthly rate, membership pausing, and 90-day money-back guarantee. Whether you need complete credit recovery or dispute a few records, they are a great choice.

Pros

- Only $79/month and you won't be charged any additional fees

- Offers a 90-day money-back guarantee

- Customer service of the highest quality

Cons

- Fees for initial work are high

- Available in some states, but not all

Pricing

There is no sign-up fee for new users, but Sky Blue Credit charges $79 to review and set up your membership after six days. They also charge an additional $79 a month starting the seventh day of membership.

Sky Blue Credit is a powerful solution to dispute errors on your credit reports, rebuild your credit, and optimize your scores.

- You will not be charged any additional fees

- Low monthly price

- Offers a 90-day money-back guarantee

- Customer service of the highest quality

- Fees for initial work are high

- Available in some states, but not all

4. Credit Strong – Best for growing savings

With Credit Strong, you can improve your credit through a savings account, but it has some important differences. Credit Strong helps people build credit through installment loans. Instead of giving the money to you all at once, they deposit it into a savings account. After that, you'll make fixed monthly payments on this installment loan. By making monthly fixed payments you can increase your credit score.

Why we choose it

Credit Strong is unique because it not only offers a credit builder loan, but also the opportunity to grow your savings. To have excellent credit, you need to make on-time payments regularly on a line of credit. However, many people don't realize that without good credit, you'll likely never be approved for such financing in the first place. Credit Strong provides consumers with the chance to change that scenario and improve their financial outlook long-term while building savings at the same time.

Pros

- Reports to the three main credit bureaus

- No credit check is required

- Long-term payment terms up to 10 years

Cons

- The interest rates for this type of loan may be higher than a traditional bank loan

- You must have an operational bank account, debit card, or prepaid card to qualify

Pricing

Credit Strong starts at $15/mo for a $1,000 installment account or $30/month for a $2,500 installment amount reported. You can cancel at any time without any penalties.

Credit Strong helps people build credit through installment loans. Instead of giving the money to you all at once, they deposit it into a savings account. After that, you'll make fixed monthly payments.

- Reports to the three main credit bureaus

- No credit check is required

- Long-term payment terms up to 10 years

- The interest rates for this type of loan may be higher than a traditional bank loan

- You must have an operational bank account, debit card, or prepaid card to qualify

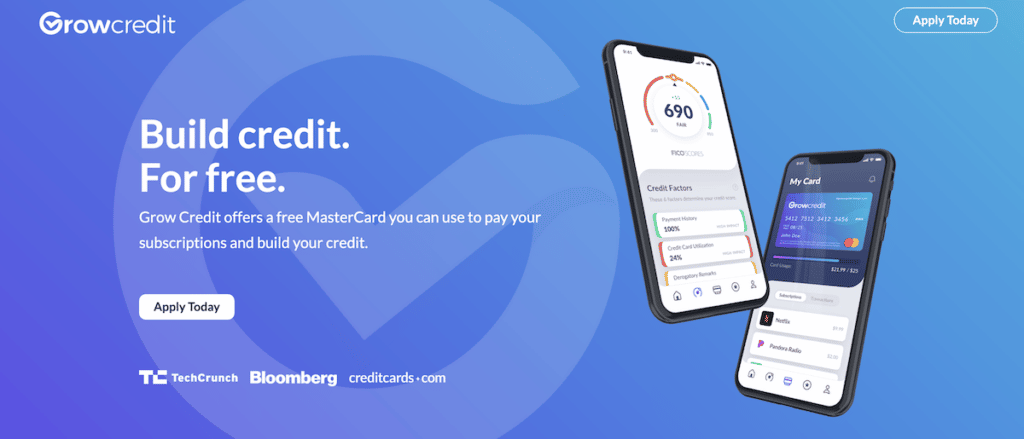

5. Grow Credit – Best free option

The Grow Credit app allows millions of Americans to build credit by automatically paying for their subscriptions through an interest-free virtual MasterCard.

Why we choose it

The Grow Credit MasterCard is free to use, which can help you improve your credit significantly. You can pay for Netflix, Disney+, Hulu, and more with the card. It is really helpful as you can leverage your recurring expenses, making it possible for you not to spend any extra money. You're only using the MasterCard to pay for things you've already paid for.

Pros

- Build a strong credit history and a diverse credit mix

- Improve and increase your credit scores between 60 and 90 days after enrolling

- A great way to build credit on a revolving basis

- Regular subscriptions can be paid for with a free virtual MasterCard.

Cons

- Only one bank account can be added to withdraw

- Paid plans require a security deposit

- Spending limits are very limited on a monthly basis

Pricing

Four pricing plans are available for Grow Credit, including the Free Build Plan, which allows users to upgrade to a paid account at any time. It's interesting to note that Grow Credit will report to Equifax, Experian, and TransUnion.

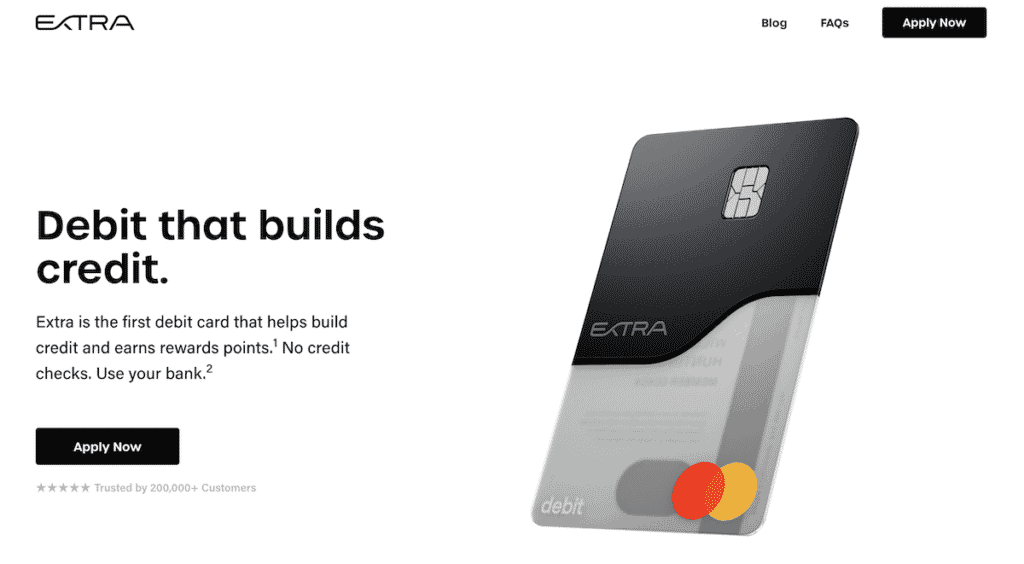

6. Extra

Extra is not a credit card – Extra is the first debit card that builds your credit. At the end of every month, Extra totals up all of your purchases and payments and reports them to credit bureaus to build your credit.

You can earn up to 1% in points for everyday purchases like rideshares, coffees and your phone bills when you upgrade your subscription to include rewards points. Users can then spend points on everything from Apple AirPods to cool products in the rewards store.

Why we choose it

The Extra credit building app is good if you don't want to use a credit card to build credit. You can easily establish credit using Extra without worrying about missed payments or interest charges.

Extra is compatible with over 10,000+ banks across the United States— so you can keep your money where you want while spending smarter with Extra.

Every time you swipe your Extra Debit Card, they spot you for the purchase and automatically pay themselves back the next business day (processing can take a couple days). At the end of each month, they send your payment information to the credit bureaus (like Equifax and Experian) that can help build your credit, as long as you keep paying them back for the purchases they’ve spotted for you.

There you have it, the very first debit card that builds your credit. Extra members raised their credit score by 48 points on average by regularly swiping and practicing good credit habits such as not defaulting on any other credit line and not utilizing too much of their total available credit.

Pros

- First debit card that helps build credit and earns rewards points

- No security deposit is required like other credit cards for building credit

- Anyone can join, no credit check or minimum credit score required

Cons

- Starts a $20 per month

- Only reports to two credit bureaus: Equifax and Experian

Pricing

Extra offers offer both monthly and annual options:

- Monthly: $20/month (Credit Building) or $25/month (Rewards + Credit Building)

- Yearly: $149/year (Credit Building) or $199/year (Rewards + Credit Building)

The Credit Building Subscription helps you build your credit, or you can upgrade to the Rewards Subscription which also lets you earn reward points for every purchase.

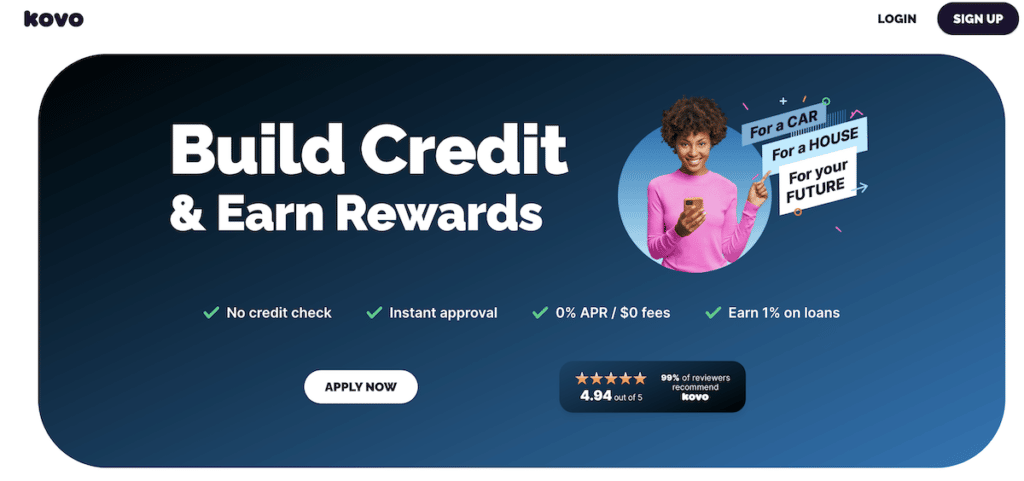

7. Kovo

Kovo is a new kind of credit builder that helps you improve your financial health and access better products and services.

By signing up to Kovo, you can build your credit easily with small monthly payments. They offer a unique way to build credit by purchasing ‘Kovo Courses' on credit, with Kovo Installments.

You would pay $10/month over 24 months for access to these courses that allow you to pick up useful skills. You can also earn with rewards with 1% back on eligible loan offers.

Payment history is the single biggest factor that contributes to your credit score, and with Kovo Installments your monthly payments are reported to the credit bureaus. What this means is that with Kovo, you can be on your way to building a stronger credit profile.

Why we chose it

Kovo offers a new way to build credit and its courses may offer valuable skills for you.

Courses are created by instructors to help you hit your goals. While these courses are all together valued at over $400, they make them available as a collection for $240.

Included are the following interactive courses:

- Job Interview Skills, Interview Strategy & Answer Scripts

- Self Confidence & Self Esteem: Confidence via Self-Awareness

- Entrepreneurship: How To Start A Business From Business Idea

- Personal Branding Path To Top 1% Influencer Personal Brand

- Stress Management With Time Management For Burnout & Anxiety

- Entrepreneurship: Sales Training, Techniques and Methods

- Ecommerce Bootcamp Academy

- Google Sheets Fundamentals

Rewards also provide a way for Kovo customers to earn gift cards when opening a loan or credit card offered by some of its featured lenders and card issuers.

Rewards are calculated as 1% of the value of a personal loan issued (up to $500 gift card), student loan issued (up to $250 gift card), student loan refinance issued (up to $250 gift card), and $75 gift card for a credit card issued.

Thus, if you are already in the market for a financial product, then it makes sense to go through them to earn a free gift card.

Pros

- Ability to build credit plus learn through courses

- Credit check not required

- Reported to Experian® and Equifax® on a monthly basis

- Instant approval with 0% APR and $0 fees

Cons

- Some people may not have time to utilize the courses

- Brand new product, not many reviews yet

Pricing

Kovo will cost you $10/month for 24 months for access to its courses. Payments are automatically run from your linked payment method.

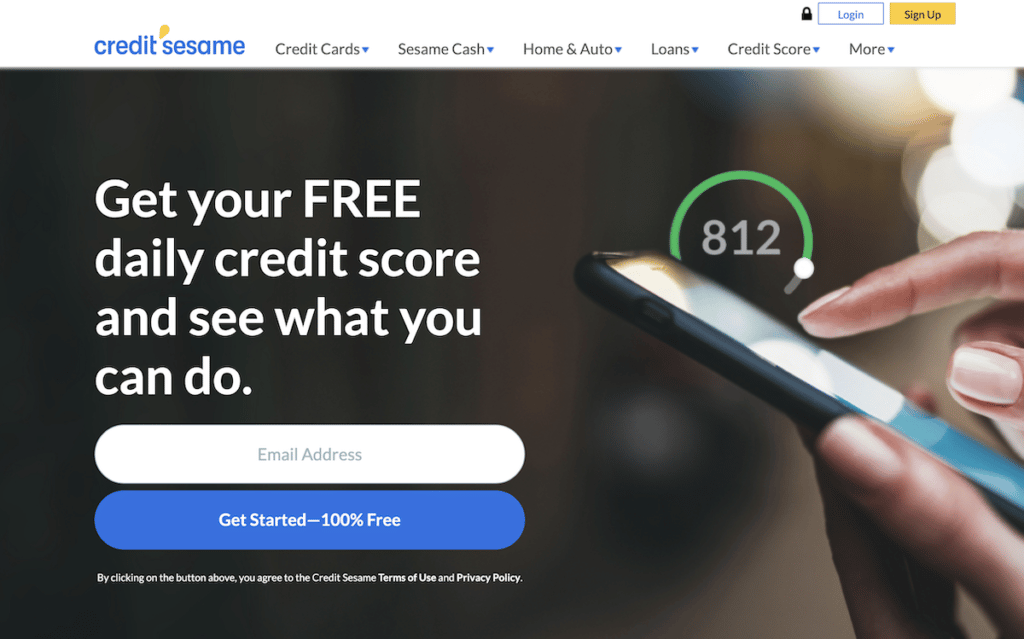

8. Credit Sesame

Credit Sesame offers free (and paid options) credit building services to people who want to improve their finances by increasing credit scores.

Why we choose it

Your credit can be managed proactively with various free tools from Credit Sesame. Although Credit Sesame offers premium tools – including access to three credit reports – they are not worth the price. Hence, to keep track of your credit score and get notified when your credit report changes, it is recommended to get at least one app that can help monitor this for you.

Pros

- Many of the most useful features of the service are free of charge.

- No-cost identity insurance for $50,000.

- Credit score improvement suggestions are offered.

Cons

- Your VantageScore is all that's shown, which isn't commonly used by lenders.

- It is only available to partners of Credit Sesame to receive product recommendations.

- There is no point in spending money on premium upgrades for the service.

Pricing

Many of the most useful features of the service are free of charge.

9. Sable

Sable is a secured credit card and bank account that you can open in just 5 minutes.

Why we choose it

Sable offers a secured credit card where you can earn unlimited cash back on all your purchases. It is also easy to use as it gives room for you to access unsecured credit after using its services for four months of on-time payments. As such, try using Sable if you truly want to elevate your credit score.

Pros

- Easy set up for autopay for on-time monthly payments

- No soft or hard credit pull

- Premium card perks

- No annual fees

- Easy account freezes

Cons

- Reviews online say their customer support isn't the best

Pricing

Sable allows you to set a credit limit equal to what you deposit. In essence, if you deposit $400, your credit limit will automatically be $400.

10. SeedFi

SeedFi is a top credit building app where you can borrow without fear, save without stress, and confidently improve your credit scores.

Why we chose it

SeedFi has an attractive feature that notifies users to avoid late payment charges and fees, thus helping users avoid low credit scores. The app has two major plans, which are:

- SeedFi Credit Builder Prime and

- Credit Builder Installment Edition

SeedFi Credit Builder Prime

The SeedFi Credit Builder Prime is free and requires no fees or interest charged. All you have to do is to create an account for a line of credit using your name and select payment as low as $10 every other week. Though access to credit is not granted immediately, you must make advance payments on the debt. In this way, once your payment is up to $500, SeedFi grants you access via a savings account where you can use the money.

The benefit of the Credit Builder Prime is that it has a rotational credit structure. This means that your account remains intact after the initial $500, and the cycle repeats itself. All you have to do is to maintain the $500 savings, and you will get access to the funds.

Credit Builder Installment Edition

For the SeedFi Credit Builder Installment Edition, the loan you can get is only $500, and you have the chance to select payments of $10 to $40 per pay period. You should note that the loan length is fixed and determined by the size and frequency of the payments you make. It only takes seven to twenty-seven months to repay the funds, with SeedFi charging about a dollar per month.

However, with the above plans, you can close the account when you feel you have reached the score benefit you need and can qualify for credit on your own.

Pros

- Good for immediate cash need

- Great for growing your savings

- No fees or interest

- Free to use

- Good for building credit

- Excellent for building a positive payment history

Cons

- Requires SeedFi savings account

- No option to choose a payment date

- No joint account or co-borrower option

- Total funds not immediately available

Pricing

For the pricing, SeedFi's “Borrow & Grow” service is where the app makes its money as they take interest charges and sell this feature to you on the app. However, Credit Builder Prime is a free service users can use on the app.

Who Should Use Credit Building Apps?

Credit building apps can be a great tool for anyone who wants to improve their credit score. However, they are especially useful for people who have bad credit or want to establish credit history. If you fall into one of these categories, then you may want to consider using a credit building app to help improve your credit score.

There are a few different types of credit building apps available. Some are designed for people with bad credit, while others are meant for people who have no credit history. There are also some that are specifically designed for people who have both bad credit and no credit history.

No matter which type of credit building app you choose, they all have the same goal: to help you improve your credit score.

FAQs

Credit history is a record of how you've managed to repay debts, such as credit cards and loans. Your credit history is recorded in your credit reports, containing additional information about your finances. You'll need to check your credit report to see if you need to remove any closed accounts or negative payment history and more.

Building a good credit score helps to ascertain if lenders will grant you loans or not. It helps you secure interest rates on mortgage and personal loans.

Credit building apps are a good idea once you notice a low credit score.

A credit builder loan is different from a traditional loan. With a traditional loan, you might receive the money you're borrowing upfront and pay it back over time. But with a credit builder loan, you make fixed payments to a lender and then get access to the loan amount at the end of the loan's term.

Best Credit Building Apps Summary

No doubt, it can be said that there is increased pressure on individuals seeking to boost their credit scores, as low credit scores determine if a lender will grant loans out to you or not.

To handle such a challenge, it would be helpful to use a credit building app to help identify your problem areas with finances and improve your credit score.

With this in mind, this article encourages you to examine the following best credit building apps to help determine how you can approach credit handling.

In a perfect world, we would all have great credit scores. But if you need to increase your credit score significantly — then credit builder apps can help you.

Credit builder apps help you improve your credit score by offering free credit monitoring, access to a line of credit or credit building loan. By making on-time payments and keeping your balance low, you can improve your credit score over time. And the best part is, there are many credit builder apps available for free.

{kind=link}