“A penny saved is a penny earned,” or so the saying goes. But when it comes to choosing a savings account that will make the most of your pennies, nickels, and dimes, reading the fine print makes a huge difference. The higher the interest rate you can find, the more your savings will accrue to build wealth over time.

If you’re looking into savings accounts, we’ve got a list of the top-earning accounts from various financial institutions. Some offer better interest rates than others, but they’re all above 5%. And with that kind of interest rate, the pennies you save today could easily grow into dollars down the road.

Ready to start saving big? Here are seven high-yield savings accounts you should consider that offer a 5% (or more) interest rate. You can see our favorites below.

2025's Top Savings Accounts – High Yield Deposit Accounts

Best 5% Interest Savings Accounts

- Current: 4% up to $6,000

- Digital Federal Credit Union: 6.17% up to $1,000

- Blue Federal Credit Union: 5.00% up to $1,000

- Landmark Credit Union: 7.50% up to $500

- T-Mobile Money: 4.00% up to $4,000

- NetSpend: 5% up to $1,000

1. Current: 4%

Current is a neobank that works differently than traditional savings accounts, far from it actually since it offers a hybrid checking/savings account.

What separates Current from other banks is that it offers 4% interest on its savings “pods” for balances up to $6,000.

Savings Pods are a way to save for whatever you want, whether that's a rainy day fund, a vacation, or even monthly expenses like groceries.

Current has different savings pods where you can deposit $2,000 in each earn to earn up to $240 in interest over the year.

This is a significant increase from the traditional 0.07% offered by most traditional banks. In addition, there are no fees associated with Current's savings account. This makes it an ideal option for those looking to save money.

Current also has a slew of other features, such as a debit card that offers cash back, overdraft protection, a debit card for kids, getting paid 2 days early, and a cash advance feature.

- Payday is just one tap away

- Get up to $750 before payday

- Get free instant access to your paycheck in advance

- No monthly fees, no catch

- Get $75 free with code PAYROLL75 and a $200+ deposit in 45 days!

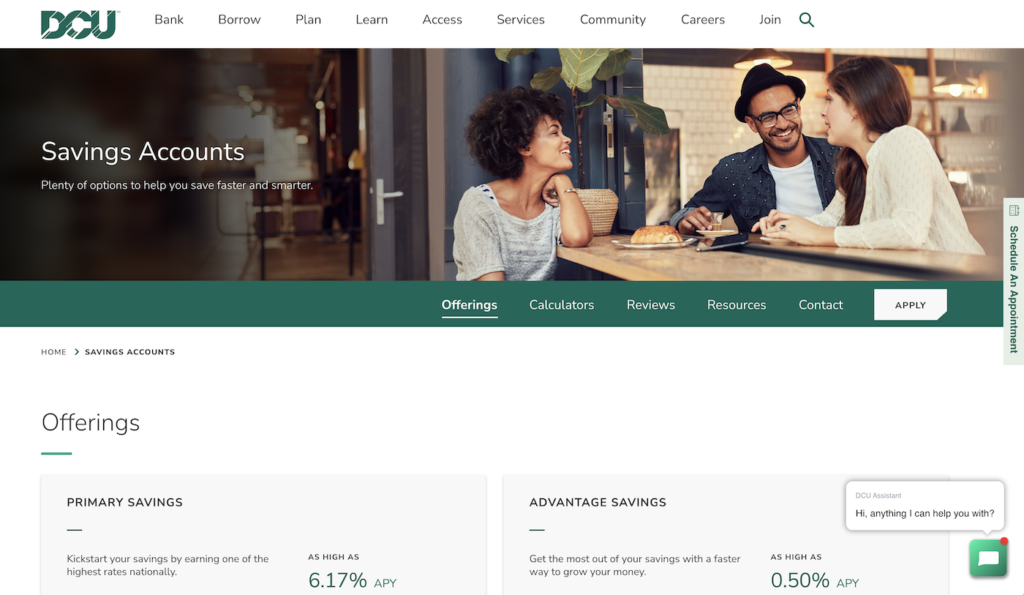

2. Digital Federal Credit Union: 6.17%

The folks at Digital Federal Credit Union offer a variety of savings accounts for various occasions. From saving for the holidays to choosing your own reason, there are plenty of opportunities to stow away your money for the right occasion.

Opening an account at Digital Federal Credit Union requires the basics, such as a government issued ID, proof of address, your social security card, funding information, and, of course, an age over 18 years. The process takes about five minutes total and can be done online.

While the Advantage Savings Account offers no minimum balance to open and no monthly fees, you’ll only earn 0.50% APY. The dividends are compounded on a monthly basis, but it’s with the Primary Savings Account that you’ll earn up to 6.17% APY on balances up to $1,000. For that account, you’ll need $5, but you won’t pay a monthly fee.

With a Digital Federal Credit Union Primary savings account, you will only earn a high percentage on the first $1,000 you deposit, but you won’t be cutting into those savings with a monthly fee. Plus, they offer many other financial services if you’re looking to keep your transactions within the same institution.

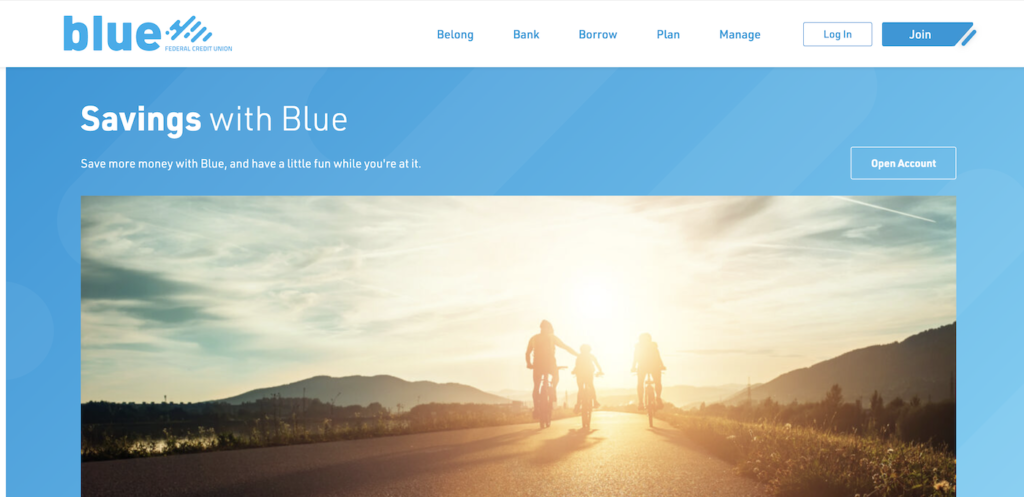

3. Blue Federal Credit Union: 5.00%

If you’re looking for a straightforward savings account that makes squirreling away money an easy task, look no further than Blue Federal Credit Union. This particular financial institution works off a tiered system, offering 5% interest on the first $1,000 saved. After that, the tiered APY ranges from 1.8% to 0.15%. Plus, you won’t have to fulfill any requirements in order to earn this 5% APY.

In fact, all you need to open an account at Blue Federal Credit Union is $5 and the typical slew of personal information. An email address begins the process, along with an ID, social security number, and an answer to the decision whether you want to add a joint owner or not.

One of the best things about a savings account at Blue Federal Credit Union is that you can make deposits and withdrawals at any time. With the tiered structure, you do have the ability to earn a respectable APY on your balances.

While there aren’t necessarily any other perks to the Blue savings account, there are a few other types of savings accounts you can open as well. Check out more of Blue Federal Credit Union’s savings accounts to see how much you can earn for your savings.

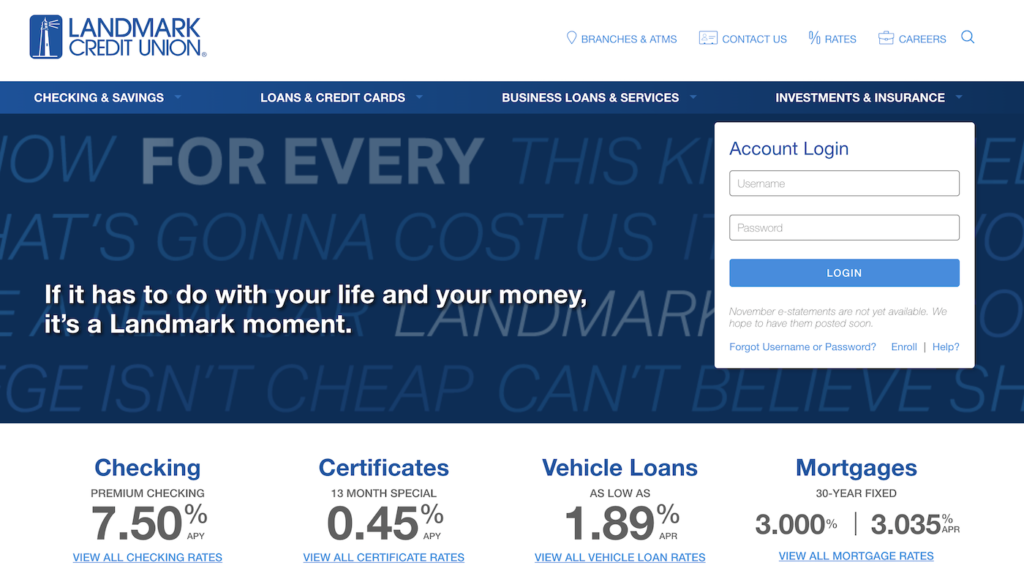

4. Landmark Credit Union: 7.50%

Like many other savings accounts on our list, this one from Landmark Credit Union requires a minimum $5 balance to open. You’ll also need an ID, social security number, and a few other bits of personal information.

However, Landmark Credit Union does not charge monthly fees for their savings accounts. The entry-level savings account is called VIP savings and will only earn you 0.10% APY on your balance. If you choose the Signature Money Market savings account, however, you’ll gain access to an interest rate of up to 0.04%. You can also open a premium checking account that offers a 7.50% APY.

Unfortunately, though you only need $5 to begin an account, you will only start earning interest on a $25 balance. That does force you to put a bit more into the pot, but it can increase your savings over time.

5. T-Mobile Money: 4.00%

You may think of them as only a cell phone company, but T-Mobile does offer more. In fact, you can open an online checking account with them. Though it might not be a traditional savings account, it can still save you money.

Signing up for a T-Mobile Money account takes just a few minutes. You’ll gain access to over 55,000 free ATMs and won’t pay any account fees. Plus, you can get your paycheck 2 days early with direct deposit and T-Mobile covers you up to $50 in overdraft protection.

Everyone earns 1% APY on all balances, but in order to earn high interest on your balance, you’ll have to make at least 10 qualifying purchases per month. Then, you’ll earn up to 4% APY on balances up to $3,000 and 1% APY on all balances after that.

6. NetSpend: 5%

If you aren’t already a part of the NetSpend family, you’ll have to join in order to take advantage of their savings accounts’ perks. Opening an account requires no minimum balance and no credit check, plus there’s no activation fee either.

In order to earn the 5% APY available, your average daily balance must be $1,000 or more. If it’s over $1,000, you’ll earn 5% APY on the first $1,000 and 0.50% on the remaining balance.

NetSpend allows you to transfer money to and from your checking and savings accounts for free. However, you can only make up to six transfers per month. You can also sign up for Autosave to automate your savings.

FAQs

Yes! The seven institutions we’ve listed above all pay 5% APY on their savings accounts. You can also check with your existing bank to see if they offer a savings account with a 5% interest rate.

Mango Money offers 6% APY on their savings accounts. In comparison, this rate is much higher than offered at traditional banks like Goldman Sachs, Bank of America, American Express, Citibank, Axos Bank, Ally Bank, Vio Bank, Synchrony Bank, CIT Bank, Barclays Bank, and other traditional brick and mortar banks.

If you’re looking for the highest interest rate, Mango Money is the bank you’ll want to contact. There are other ways to obtain high interest on your money, including many investment opportunities.

A high-yield savings account is an interest-bearing account that typically pays a better rate of return than a traditional savings account. Although the exact amount varies, the national average of high yield savings accounts generally offer an annual percentage yield (APY) between 0.04%. These banks listed on this post all offer 5% or more which is rare.

What to Look for in a Savings Account

As you compare savings accounts, look beyond just the interest rate to consider the following factors.

Interest rate and APY

Savings accounts can easily be distinguished by the annual percentage yield (APY), which is often expressed as an interest rate. For example, our list of seven savings accounts all have an annual percentage yield of 5%, which means you’ll earn 5% interest on your balance over a year’s time.

As you can imagine, a higher APY interest rate will do more to compound your savings over time. Earning 5% APY may not seem like much, but it’s better than not earning interest on your money at all. This is especially true for money that’s stashed away and/or not invested.

Initial deposit

Very rarely will you find a savings account that doesn't require some sort of minimum deposit requirement. That being said, there are plenty of savings accounts out there that keep the bar low, at anywhere between $10-25. Most banks will require an opening deposit at the time of the opening of your account, so make sure to budget for that up front.

Minimum balance requirements

Along with an initial investment, many banks require you to hold a certain minimum balance within the account. Dipping below this number may not have any short-term effects if you’re able to restore that balance, but be sure to read the fine print, especially if you’re saving in a low-income household.

Account fees

Saving on bank fees can be a great way to not only improve your budget but add to your savings balance as well. Savings accounts can incur account fees for particular actions, such as transferring money more often than is allowed for free. As you look at savings accounts, investigate potential cases for these account fees and any monthly maintenance fees and keep them in mind if you do sign up.

Rate tiers

Saving money is all about building up that balance. But if you’ve got a sizable deposit to make, some banks will reward you differently for a larger balance. Typically, banks will structure APYs into a tiered system, which pays more or less depending on how much you’ve put into the account.

Accessibility and ease of use

Building an emergency fund with a savings account doesn’t always mean you have to go into a brick-and-mortar bank to open an account. In fact, there are plenty of online savings accounts available. While opening a savings account at an institution you’re already a member of could allow you to exchange money between your checking and savings accounts, having a dedicated online savings account could streamline your savings plan, too.

FDIC insured

The Federal Deposit Insurance Corporation (FDIC) is a government agency that was created in 1933 to protect consumers' money in case of a bank failure. The FDIC insures deposits up to $250,000 per depositor, per bank.

Deposits are a key part of the U.S. financial system, and they are one of the most important ways that consumers can protect their money.

When you deposit your money in a bank, that money is insured by the FDIC. This means that if the bank fails, your money is still safe and you will get it back.

Save Today to Earn Tomorrow

Opening a savings account is a great way to plan for the future, unexpected or not. We hope you’ve found this list of the best high-yield online savings accounts with 5% APY useful in your search. It’s never too early (or late) to start saving, and earning more for those saved dollars pays off down the road. The same dollars could help improve your financial future in various ways, many of which we discuss in our other posts.

Check out more of our articles for financial tips and stay tuned for new content:

- 13 Simple Ways to Get Out of Debt

- 10 Best Budgeting Apps

- 9 Best Apps to Save Money on Groceries

- How to Save Money on Your Next Cruise

{kind=link}